Over the last ten years, free ad-supported streaming TV (FAST) services have established themselves as a free access point to older shows, with channels dedicated to the likes of Baywatch, Murder She Wrote and even Pimp My Ride. But research from Gracenote, Nielsen’s content division, reveals that FAST content is actually getting younger. According to the service’s analysis of the FAST channels in its global video database, more than 70 percent of FAST content was produced post-2010, and just 13.4 percent pre-1990.

The trend comes with an explosion in FAST channels, with more than 1,500 different channels available globally – an increase of 42 percent over the last two years. Dave Bernath, compares this evolution in content to the path of cable TV, which was also once home to older library content.

“Cable in the US was initially relying solely on older content, proven shows, sitcoms, movies and procedurals,” Bernath tells VideoWeek. “And the playbook of basically relying on solid library IP to get these channels off the ground has kind of repeated itself.”

The difference is that cable channels are paid by distributors each month, who started pushing to get more value for their carriage fees, resulting in new content made for cable TV channels such as MTV and Nickelodeon.

“We don’t have that dynamic in FAST, because it’s all free,” says Bernath. “But what we do have is improving content; instead of 20 years old, it’s ten years old. And so you’re seeing the age and recency of content start to move up the value chain, which is really exciting.”

Reality bites

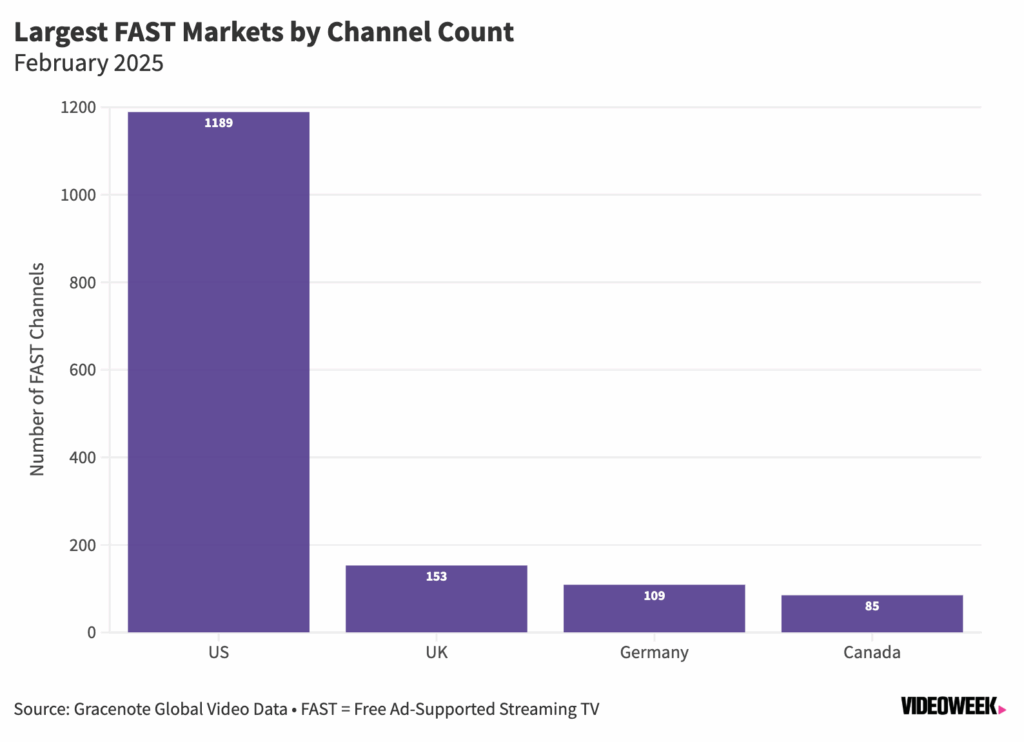

Like cable, FAST services have taken a particularly strong foothold in the US due to the absence of a free TV ecosystem. The US is home to 77 percent of the FAST channels available globally, according to Gracenote, dwarfing the number of channels available in the next largest FAST markets: the UK, Germany and Canada.

“Europe has a much more robust free ecosystem through the public broadcasters in the various countries,” comments Wurl’s Bernath. “We don’t have that dynamic in the States, thus the rise of cable, and now subscription services. This has given FAST a slightly slower development in Europe; there’s still a lot happening, but it’s still relatively small and nascent compared with the US.”

And this relative youth also skews the age of FAST content in the newer markets, according to the Gracenote data. In the UK, 79 percent of FAST content was produced post-2010, rising to 80 percent in Germany – compared with 74.5 percent in the US. Again this reflects the earlier establishment of FAST channels in the US, which were initially populated with older content. But FAST channels in the UK and Germany have emerged more recently, and are therefore more likely to house newer content.

Meanwhile that newer content is reshaping the makeup of FAST channels. Just as the start of original programming on MTV ushered in the dawn of reality TV in the 1990s, reality content is now “the biggest mover in FAST”, according to Gracenote, with the number of reality channels growing 626 percent in the last year alone. And looking at the UK, Ampere Analysis reports that unscripted content accounts for 60 percent of the newer titles (less than five years old) airing on the FAST service Pluto TV.

This shift serves to bolster the position of FAST channels as the linear-like, “lean-back” alternative to SVOD services, as the content tends to be “underserved” by the paid subscription services. Gracenote notes that entertainment content makes up just 1.6 percent of SVOD content, compared to 3.9 pecent of FAST content. Meanwhile in the UK, unscripted documentary and reality channels account for 12 percent of the total channel availability.

The next wave

The other genre racing onto the scene is sport, according to Gracenote, with 220 sports channels available globally, including those dedicated to the NFL, MLB and PGA Tour. Roku also launched a premium sports FAST channel last August, while Fox offered a free livestream of the Super Bowl on Tubi in February.

Gracenote observes that sport is another genre “in short supply” on SVOD services. Sports channels now make up 13.6 percent of FAST channels globally, whereas sports programming accounts for only 1.3 percent of content across Prime Video, Apple TV+, Disney+, Netflix and Paramount+.

However, these channels tend to focus on replays and highights, or archive and documentary content, due to live sports rights being tied up in expensive, exclusive deals with major broadcasters and streaming services. But Wurl’s Dave Bernath suggests more live sport will come to FAST services, particularly for niche sports which, again, may be underserved by other streaming services.

“Sports will be the last category to really get to a higher level,” he says. “The Premier League, the NBA, the NFL, these are all tied up in massive economic deals that are moving into streaming, but they tend to be on Prime, Netflix or Peacock; it’s not something free on Samsung TV Plus. But more niche sports are less expensive, so there’s more and more live coming.”

The other missing piece of the FAST picture is exclusive or original content; a major selling point of the SVOD services, but slower to materialise on FAST channels, which are themselves rarely exclusive to individual services or platforms. And while more recent content is making its way onto FAST channels, Josh Rustage, Senior Analyst at Ampere Analysis, says the ecosystem is still primarily used “to extract further value from library content that has expended value elsewhere.”

“It took a long time for the cable industry in the US to start investing in originals,” adds Bernath. “We’ll slowly start to see that in FAST as well, but at the moment, the economics aren’t necessarily there.”

Follow VideoWeek on LinkedIn.